1. Indo -China trade relations and industry study for chemicals sector

Asia and Chemicals Industry

Asia’s economies are among the world’s fastest developing. The increased use of cosmetic and personal care products in Asia has had an especially significant effect on formulating firms, as they too hope to benefit from the region’s growth. Performance-enhancing chemicals were regarded as corrective agents for weaker formulations thirty years ago. Emulsifiers, viscosity inhibitors, specialty surfactants, and other additives are now considered essential components of high-performing, low-cost consumer goods.

Deregulation in developing markets has resulted in an increase in GDP, which has led to an increase in generic use, which has resulted in an increase in demand for specialty chemicals (Fost, 1997). Asia’s share of total specialty chemical demand is expected to rise from around 47% in 2018 to 50% by 2025, fueled disproportionately by China and India. Analysts agree that India has a great opportunity to grab market share from China by utilizing its assets, which includes a stable reformist political leadership, a growing consumer demographic, and a startup culture with higher English language proficiency than its Chinese counterparts (Singh, 2020).

Chemical Industry of India

IBEF on behalf of the ministry of Commerce and Industry of India comments that the size of specialty chemicals market in India is poised perfectly for growth. This is no surprise since India is the fastest growing major specialty chemicals market in the world. Chemicals make up a considerable part of India’s total trade flow, ranking third in imports and fourth in exports over the past five years. India currently has a $15 billion chemical trade deficit. The country’s trade deficit with China fell to $45.91 billion in 2020 from $56.95 billion in 2019 (UN Comtrade Database, 2020; Suneja, 2021).

The Indian chemicals industry was valued in 2019 at US$ 178 billion. However in just the next 5 years by 2025, analysts expect the number to reach US$304 billion at a CAGR of 9.3% fueled by higher consumer demand and also a shift from the currently existing China due to trade wars, pollution laws and motivation to lower dependency aggregation after witnessing complete halt during 2020 pandemic lockdown in global manufacturing due to china being the biggest hub. Out of this, specialty chemicals constitute 22% of the total chemicals market in India and expected to rise 12% CAGR till 2022 (IBEF, 2020). Between 2006 and 2019, the compound annual growth rate (CAGR) in TRS for India’s chemical companies was 15 percent—a figure much higher than the global chemical-industry return, with a CAGR of 8 percent, and the overall global equity market, with a CAGR of 6 percent. Even between 2016 and 2019, when India’s economy faced headwinds, the chemical industry maintained a CAGR of 17 percent (McKinsey Report, 2021).

Chemical trade value has increased at a faster rate than India’s average trade value. Chemical exports increased by 11 percent from 2014 to 2018, compared to just 0.4 percent for India’s average exports, implying enormous potential in global markets, while chemical imports increased by 5% in the same period. Despite higher export growth than import growth, India still imports more than it exports, resulting in a USD 15 billion chemical trade deficit (McKinsey Report, 2021). Specialty chemicals are the most important chemical export category in India, accounting for over half (55%) of total chemical export value in 2018.

Despite this, they account for just 3% of the overall volume of specialty chemical exports globally, compared to 13% for China, 11% for Germany, and 5% for Japan. There is still scope for improvement (McKinsey Report, 2021). Additional support, in terms of fiscal incentives, such as tax breaks and special incentives through Petroleum, Chemicals and Petrochemicals Investment Region (PCPIR)s or Special Economic Zones (SEZ)s will enhance production and development of the industry. With this in mind, the government has created a 2034 roadmap for the chemicals and petrochemicals sector to look at ways to increase domestic demand, reduce imports, and encourage investment in the sector (IBEF, 2020).

The top segments in India under the specialty chemicals segment are textile chemicals, agrochemicals, specialty polymers and surfactants. Other segments expected to grow rapidly are flavouring and fragrance agents, cosmetic chemicals, adhesives, water management chemicals and food additives. All these are banking on growth fueled by forecasts of rising market demand and shift from outsourcing to import aligned with make in India movement (McKinsey Report, 2021).

India’s advantages:

1. Rising Demand

a) In India’s specialty chemicals sector, the demand from end-user industries such as food manufacturing, personal care, and home care is propelling the growth of various segments.

b) Strong demand for specialty chemicals in the automobile, personal care, water treatment, and construction segments is likely to be supported by a growing middle-class population.

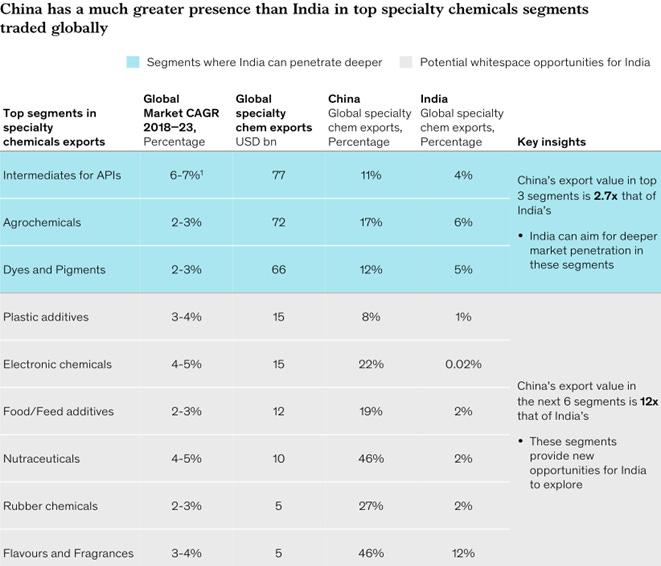

c) In the top three specialty chemical export markets – agrochemicals, dyes and pigments, and intermediates for active pharmaceutical ingredients(API) – India already has a good foothold (McKinsey Report, 2021)

2. Opportunities:

a) As multinational businesses aim to de-risk their supply chains, which are heavily reliant on China, India’s chemical industry has the potential to expand significantly.

b) The imposition of tighter environmental regulations in China, which resulted in the closure of over 40,000 units, could open doors for Indian chemical suppliers to service foreign players. Due to tougher environmental regulations, tighter funding, and restructuring, the architecture of China’s chemical industry is shifting.

c) The latest trade wars between China, Europe, and the United States have had an impact on bilateral trade, presenting prospects for Indian players to overcome the supply chain gap.

3. Policy Support

a) The government intends to implement a production-linked incentive (PLI) scheme to encourage domestic agrochemical manufacturing with 10-20% performance incentives

b) The Department of Chemicals and Petrochemicals received Rs 218.34 crores (US$ 28.97 million) in the Union Budget 2020-21.

c) With a few variations, such as toxic substances, the automatic route allows 100 percent FDI in the chemicals industry.

d) Between April 2000 and September 2020, total Foreign Direct Investment (FDI) inflows into the chemicals (other than fertilisers) market totaled USS 18.06 billion.

e) Make in India: Two major initiatives exist under Make in India that can help specialty chemicals:

i. PCPIRs (Petroleum, Chemicals & Petrochemicals Investment Regions) are clusters created by the Indian government to provide investors with a transparent and investment-friendly policy and facility framework. PCPIRs have world-class infrastructure and a competitive environment that makes it much easier to set up a business. The total expenditure needed to fully realise PCPIRs is estimated to be INR 7.63 lakh crore.

ii. CPDS – The Chemicals Promotion Development Scheme aims to promote and expand the chemical and petrochemical industries by providing financial resources for lectures, workshops, exhibits, undertaking studies/consultancies, and analysing important issues concerning the chemical and petrochemical industries (Make in India, 2020).

4. Increasing Investments

a) Specialty chemical companies in India are expanding their capacity to meet growing demand from both international and domestic markets. PCPIRs are projected to draw US$ 104.36 billion in investments.

b) Trade agreements reflect this change in interest from China to India. Strategic investors, led by Japan, Korea, and Thailand, have shown a strong interest in Indian companies in the sector since November 2020, as they look for diversification avenues for their supply chains, away from China. This included major transactions in FY 2020, such as Carlyle’s US$ 210 million acquisition of SeQuent Scientific Ltd and KKR’s $414 million purchase of JB Chemicals and Pharmaceuticals Ltd.

With these insights in mind, current scope for growth:

As data suggests, in the top 3 global segments namely API Intermediates, Agrochemicals and Dyes and Pigments, China’s export value is 2.7 times higher than India’s and thus has potential for India to seek deeper penetration into these high volume segments. In the other segments where China’s export value is 12 times higher than India’s, there room for India to explore how to break into these product segments especially in Nutraceuticals and Flavours & Fragrances segments where China holds a whopping 46% market share in both while India only has 2% and 12% export value share, respectively. Getting a foothold in these segments will lead to immense value creation specifically for the reasons of other global players trying to de-risk from Chinese supply chains.

This is an excerpt of the Chemicals industry. Full paper about Indo-China trade and pharmaceutical sector can be found on my LinkedIn page.

Disclaimer: The opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice. Nothing on this Blog constitutes investment advice, performance data or any recommendation that any security, portfolio of securities, investment product, transaction or investment strategy is suitable for any specific person. From reading this Blog we cannot assess anything about your personal circumstances, your finances, or your goals and objectives, all of which are unique to you, so any opinions or information contained on this Blog are just that – an opinion or information. You should not use this Blog to make financial decisions and we highly recommended you seek professional advice from someone who is authorised to provide investment advice.